Is Intel Stock a Hidden AI Winner?

/Intel%20Corp_%20logo%20on%20mobile%20phone-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

Once a titan of the semiconductor industry, Intel (INTC) has struggled in recent years to keep up with rapidly evolving competition, particularly in the burgeoning field of artificial intelligence (AI). It has lost manufacturing leadership to Taiwan Semiconductor (TSM) and has lagged behind the AI revolution led by Nvidia (NVDA) and Advanced Micro Devices (AMD).

However, recent developments imply the company may be quietly preparing for a significant turnaround. Its second-quarter results show a business undergoing significant transformation under a disciplined new leadership team and a renewed emphasis on AI. Intel stock is up a mere 1.94% year to date, but analysts expect 200% upside from current levels.

Let’s find out if Intel could be a hidden AI winner and if it is worth buying now.

Intel Showed Resilience Amid Its Transition

The tech giant is attempting a high-stakes turnaround, relying on its cutting-edge 18A process node, upcoming products such as Panther Lake and Nova Lake, and a complete repair of its internal culture and customer relations. Intel reported a stronger-than-expected second quarter, with $12.9 billion in revenue, exceeding consensus estimates by $977.2 million and remaining flat year over year. This performance was aided by strong demand in Intel’s Client Computing Group (CCG) and Data Center and AI (DCAI) divisions, its two largest revenue drivers.

Intel Foundry’s Q2 revenue of $4.4 billion, while down 5% sequentially, is gaining traction as the company ramps up Intel 18A, its next-generation process node. According to a Reuters report earlier this month, Intel CEO Lip-Bu Tan intends to transition from the 18A manufacturing process to the 14A process. During the Q2 earnings call, Tan stated that the 18A node is expected to support the next three generations of Intel client and server CPUs. The company intends to release Panther Lake, the first major 18A-based CPU, by the end of the year. Once internal volumes show strong yield consistency, Intel hopes to convert them into an external foundry business.

Tan acknowledged previous errors with 18A and stated that these lessons are already being applied to 14A. He stated that external customers are now involved in the early stages of 14A development. Tan also made it clear that Intel will not rush into developing or deploying its next node, 14A, until there are clear signals of yield maturity, customer demand, and economic viability. Intel is being cautious with capital expenditures, with a 2025 net capex forecast at $8 billion to $11 billion, a significant decrease from previous years. The goal is to achieve long-term sustainable profitability through scale, efficiency, and better product design. The company reported an adjusted loss of $0.10 per share in Q2, compared to a profit of $0.02 in the prior year quarter. Analysts expect 2025 to be a profitable year, with earnings of $0.13 per share, rising by 445% to $0.49 in 2026.

AI Tailwinds Begin to Show

Intel was slower to embrace the AI wave than its competitors. However, it is now focusing its strategy on the growing AI opportunity. In Q2, it launched several AI PCs with OEM partners, powered by Arc GPUs, intended for inference and professional use. Additionally, Xeon 6 processors are increasingly being used for AI workloads. Tan admitted Intel’s long-standing weakness in software and system-level solutions. The company is now prioritizing the creation of a full-stack AI platform. This will include middleware, frameworks, and developer tools that are optimized for inference, agentic AI, and edge AI.

Intel’s road to recovery is far from over. It is still way behind Nvidia in data center GPUs. Plus, AMD continues to compete in both CPUs and AI accelerators, and ARM-based chips are making inroads into the PC market. Any misstep might revive investor and customer doubts about the company’s turnaround story. Patient investors who can handle the short-term volatility may find Intel a good buy now, as the potential upside could be substantial if Intel succeeds.

Is INTC Stock a Buy, Hold, or Sell on Wall Street?

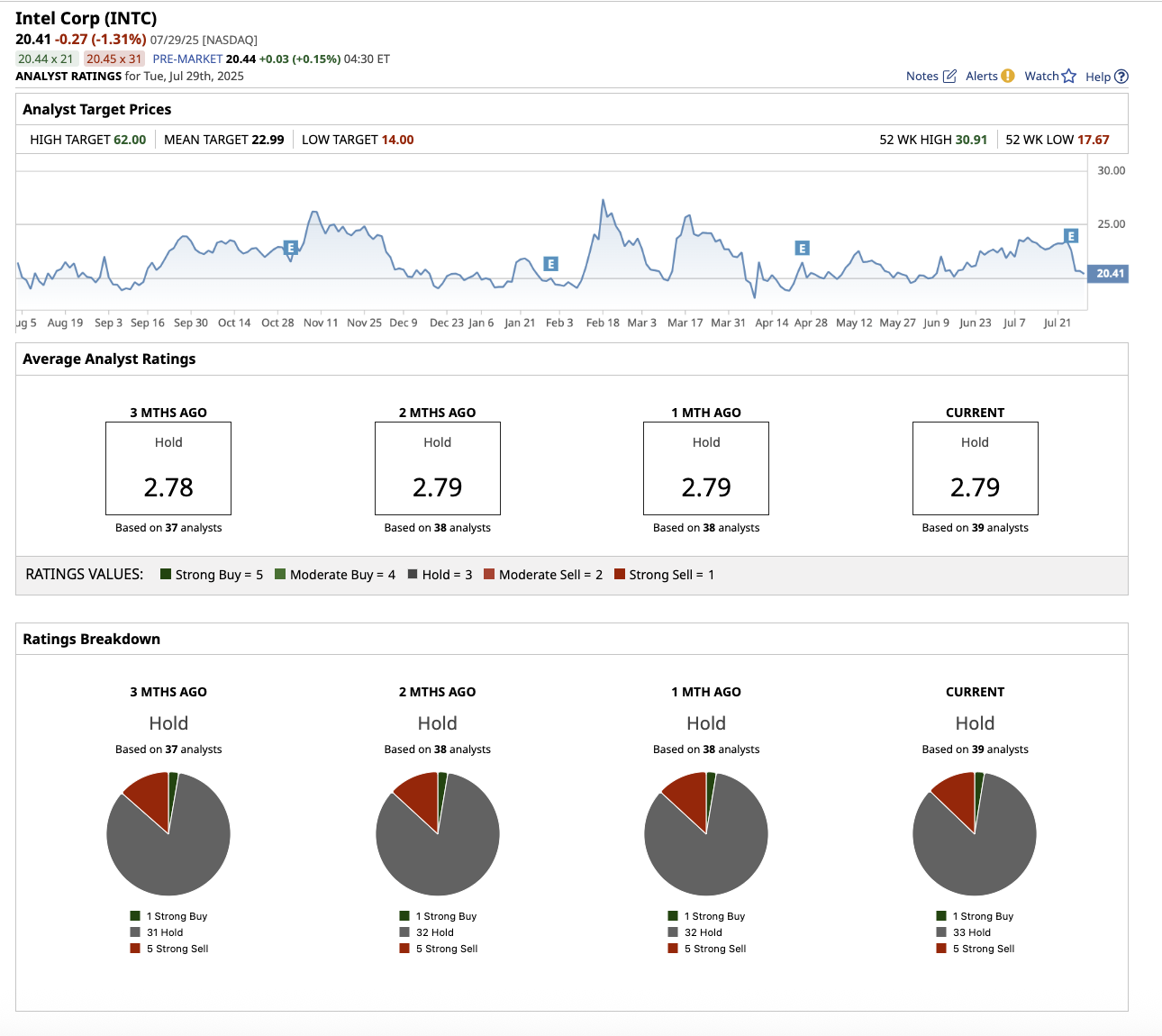

Overall, Wall Street rates INTC stock a “Hold.” Of the 39 analysts covering the stock, one rates it a “Strong Buy,” 33 rate it a “Hold,” and five suggest a “Strong Sell.” The stock is trading close to its average target price of $22.99. However, the Street-high estimate of $62 suggests the stock has an upside potential of 203.7% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.